You are an uncommitted, single and independent young professional who has just turned 30. Self-sufficiency is the name of the game – you have stable income from your dream career, you’ve just paid off your car loan and you can splurge intermittently on fashionable Nine West shoes and Calvin Klein dresses.

However, there is one piece of life’s puzzle which doesn’t fit – you still live with your parents. While this allows you to revel in countless benefits like free laundry facilities, companionship and most importantly, readily available food supplies, you are at that individualistic stage where you are coming to your own. You feel that niggling need to decorate your own space and to entertain at your discretion, without requesting permission from a third party. You have decided that it’s time to move on and move out and visit local real estate sites to identify key comfortable residences. You contemplate, “should I explore the rental section or should I bite the bullet and buy my dream location.”

At the age of 30, it is highly unlikely that you are liquid enough to buy a place without getting a mortgage. Simply put, a mortgage is a property loan which is repayable over a set number of years. The creditor’s security for this loan is the property acquired. Therefore, if your monthly payments cease, the creditor has the right to seize the property from you.

Renting, on the other hand, involves the payment of a fixed monthly fee to a landlord for tenanting his property. This payment is governed by a rental contract, which is usually renewable at the end of a fixed term (normally one year).

The key features of each option which you should consider include:

Mortgage and Rental Agreements Comparisons

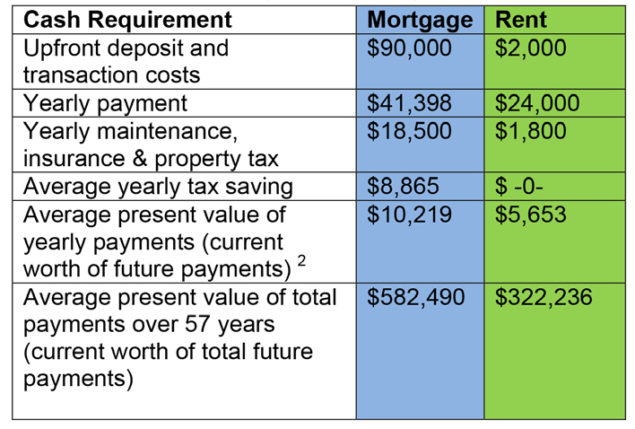

Evidently, from Table 1 above, a mortgage requires you to have a higher and steadier cash inflow. The current price of a 2-3 bedroom house on the island, ranges from EC$500,000 – $1,000,000. Under a rental, the minimum rate for a modern, well-kept and well- located 2-3 bedroom residence ranges from EC$1,500-$3,000. Let’s say you decide on a 2 bedroom modern apartment, with the following mortgage and rental characteristics:

Mortgage vs Rental Scenario

Over your remaining 57 years, the cash flow impact per option will be as follows:

The above computations scream out that it is more economical to rent. However, you are a forward thinking, enterprising individual and realise that there are many income-generating opportunities which exist from holding a property under a mortgage. These include renting and or reselling your property at the end of the mortgage term. Clearly, you and your estate will also be enriched by a valuable asset which is transferrable to your heirs. Such avenues can bring substantial gains which would hardly be realized from the rental option. In addition, most mortgage agreements allow you to pay more than your fixed monthly payment without incurring penalties. Therefore, this can lead to a lower mortgage cost altogether.

Your decision to rent or buy rests solely on your long-term life goals and cash flow capabilities. Being young and progressive, you may decide to buy a fair-priced property and hold it for a period of time. You can then make a large profit through reselling or leasing when the local real estate market recommences an upward trend.

Fortunately, this is one of the many critical financial decisions you will have to make as a young adult. Isn’t it exciting to be one?

Nakita Edwards is the Director of DCIC Professional Services.